In Part 1 of our series, we explored the foundational concepts of responsible AI in the payments industry. In this post, we discuss the practical implementation of responsible AI frameworks.

The need for responsible AI

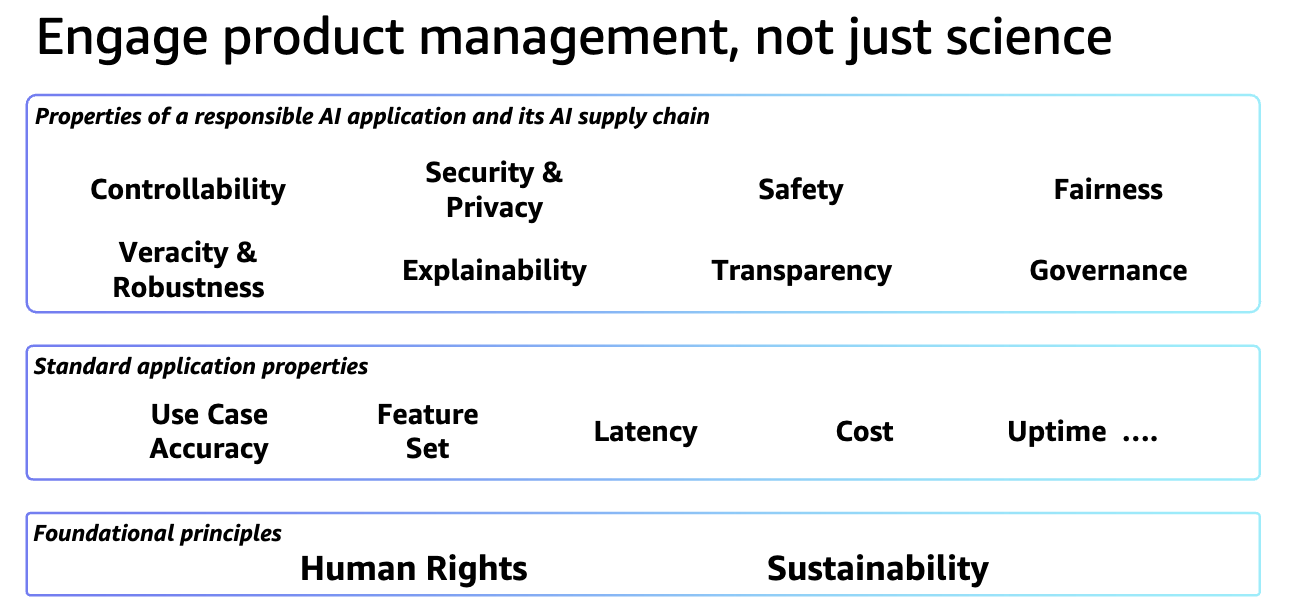

The implementation of responsible AI is not passive, but a dynamic process of reimagining how technology can serve a customer’s needs. With a holistic approach that extends beyond traditional boundaries of technology, responsibility, law, and customer experience, AI can become a powerful, transparent, and trustworthy partner in financial decision-making. Responsible AI is an additional layer and a core architectural principle that influences every stage of product development. This means redesigning development processes to include responsibility assessment checkpoints. Bias testing becomes as critical as functional testing. In addition to technical specifications, documentation now requires comprehensive explanations of decision-making processes. Accountability is built into the system’s core, with clear mechanisms for tracking and addressing potential responsibility challenges. Tenants of Responsible AI should be thought as a part of the product management and application development life cycle as highlighted in the picture below:

In the following sections, we provide several recommendations for responsible AI.

The AI Responsible Committee

Consider establishing an AI Responsible Committee for your financial institution. This cross-functional body can serve as a central hub for AI governance, bringing together experts from various disciplines to guide responsible AI innovation and support alignment with responsible AI practices.

Cross-functional oversight: Dismantling organizational boundaries

Traditional organizational structures can create barriers that fragment technological development. Cross-functional oversight breaks down these silos, creating integrated workflows that promote responsible considerations in the AI development process.

This approach might require reenvisioning how different departments collaborate. Doing so can help you integrate compliance as part of a larger AI development process, rather than as final checkpoints. In this setting, legal teams have an opportunity to be strategic partners, and customer experience professionals become translators between technological capabilities and human needs.

The result is a holistic approach where responsible considerations are not added retrospectively and are fundamental to the design process. Every AI system becomes a collaborative creation, refined through multiple lenses of expertise.

Policy documentation: Transforming principles into operational excellence

Policy documentation can help promote frameworks that guide technological innovation. These documents serve as comprehensive blueprints that translate abstract principles into actionable guidelines.

An effective AI policy articulates an organization’s approach to technological development, establishing clear principles around data usage, transparency, fairness, and human-centric design. These policies can also reflect an organization’s commitment to responsible innovation.

Responsible AI as organizational leadership

By creating responsibly grounded, adaptive AI systems, financial institutions can transform technology from a potentially disruptive force into a powerful tool for creating more inclusive, transparent, and trustworthy financial systems. Responsible AI is a continuous journey of innovation, reflection, and commitment to creating technology that helps human achieve their objectives.

Global collaborative landscape

The landscape of responsible AI in financial services is rapidly evolving, driven by a network of organizations, regulators, and industry leaders committed to transforming technological innovation to be responsible, transparent, and socially responsible. From non-profit initiatives like the Responsible AI Institute to industry consortiums such as the Veritas Consortium led by the Monetary Authority of Singapore, these organizations are developing comprehensive frameworks, governance models, and best practices that move past traditional compliance mechanisms, creating holistic approaches to AI implementation that prioritize fairness, accountability, and human-centric design.

This emerging landscape represents a fundamental shift in innovation, with regulators, tech companies, academia, and industry working together to establish AI standards while driving innovation. By developing detailed methodologies for assessing AI solutions, creating open-source governance frameworks, and establishing dedicated committees, these initiatives are mitigating risks. Additionally, this will help in actively shaping a future where AI serves as a powerful, trustworthy tool that enhances financial services while protecting individual rights and societal interests. The collective goal is to make sure AI technologies in payments are developed and deployed with a commitment to transparency, fairness, and responsible considerations. Organizations can establish dedicated mechanisms for monitoring global developments, participating in industry working groups, and maintaining ongoing dialogues with regulatory bodies, academic researchers, and responsible AI experts to make sure their AI strategies remain at the forefront of responsible technological innovation.

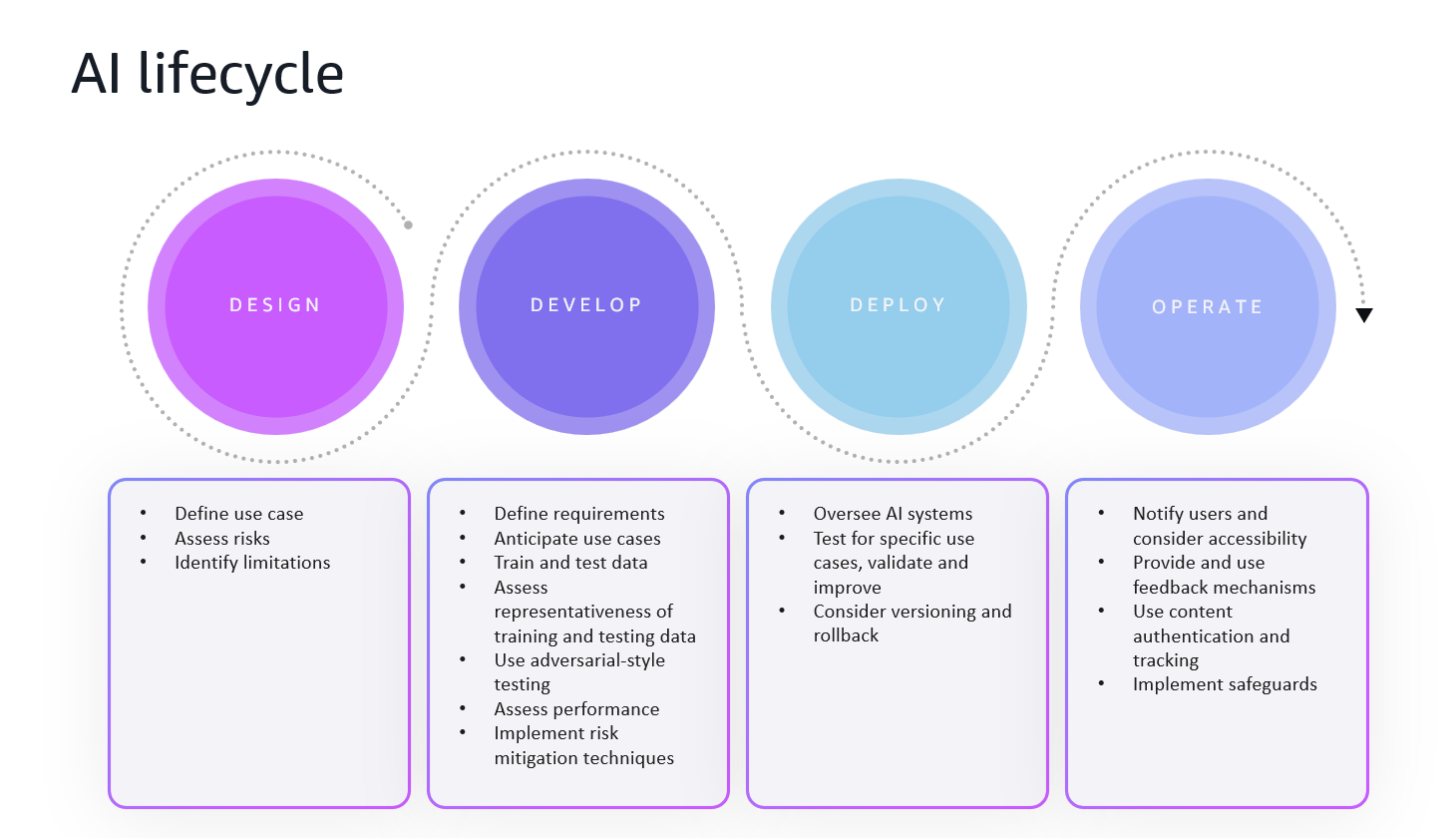

AI lifecycle phases

The following figure illustrates the different phases in the AI lifecycle, comprising design, development, deployment, and operation.

In the following sections, we discuss these phases in more detail.

Design phase

The design phase establishes the foundation for AI systems. In this phase, AI builders should consider assessing risks through frameworks like NIST AI Risk Management Framework. This includes documenting and narrowly define use cases, stakeholders, risks, and mitigation strategies while recognizing AI’s probabilistic nature, technical limitations, confidence levels, and human review requirements.

In payments and financial services, risk assessment can help identify harmful events for use cases such as fraud detection, transaction authentication, and credit decisioning systems. For example, in use cases where binary outcomes are generated, the design should carefully balance false positives that could block legitimate transactions against false negatives that allow fraudulent ones. Financial regulators often require explainability in automated decisioning processes affecting consumers, adding another layer of complexity to the design considerations.

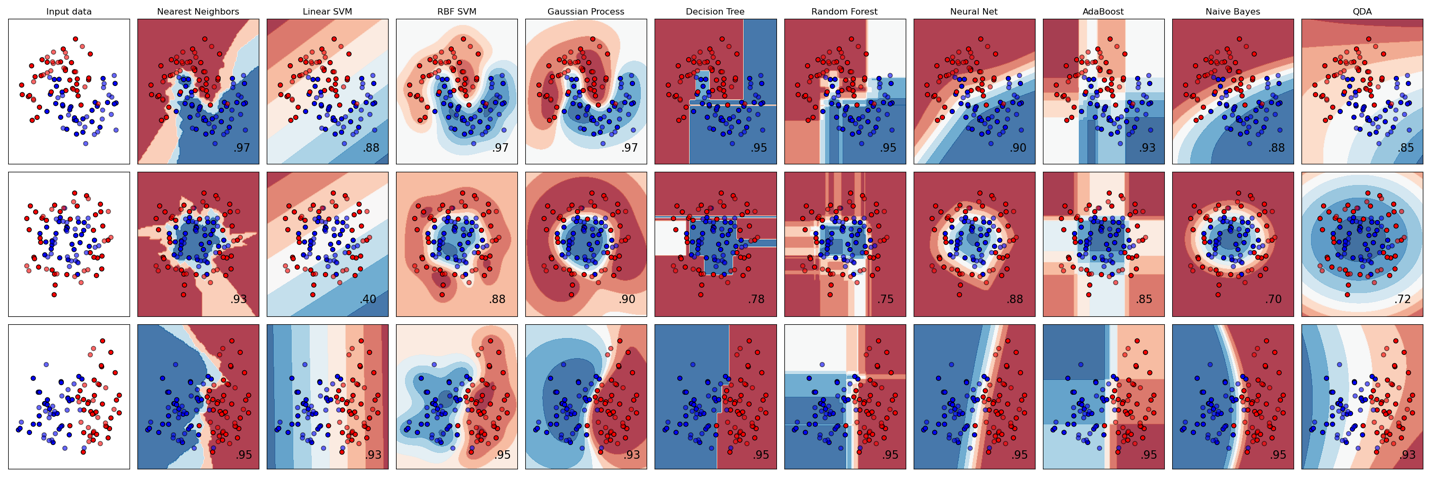

The following figure shows example of a decision boundary visualization or classification boundary plot. It’s a type of scatter plot that displays the training data points (as colored dots) and the decision regions created by different machine learning (ML) classifiers (as colored background regions). This visualization technique is commonly used in ML to compare how different algorithms partition the feature space and make classification decisions. Similar plots can help with responsible AI by making algorithmic decision-making transparent and interpretable, helping stakeholders visually understand how different models create boundaries and potentially differ between groups.

Additionally, here is visualization comparing performance of various ML algorithms.

Additionally, here is visualization comparing performance of various ML algorithms.

Development phase

The development phase involves collecting and curating training and testing data, building system components, and adapting AI systems into functional applications through an iterative process. Builders define explainability requirements based on risk levels, develop metrics and test plans, and promote data representativeness across demographics and geographies.

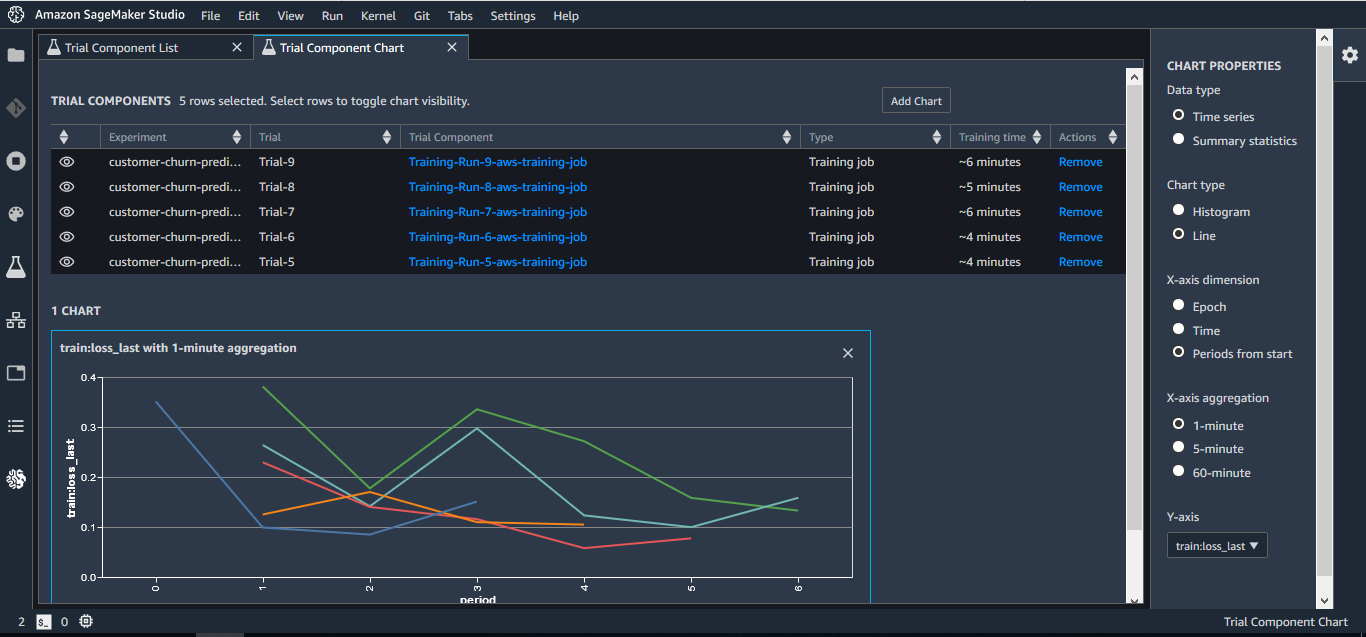

Payment AI systems specifically require highly representative training data spanning transaction types, merchant categories, geographic regions, and spending patterns. Data security is paramount, with secure storage measures to protect data. Testing should incorporate diverse scenarios like unusual transaction patterns, and performance assessment should use multiple datasets and metrics. Development also includes implementing fairness measures to mitigate bias in credit decisions or fraud flagging, with comprehensive adversarial testing (also known as red teaming) to identify vulnerabilities that could enable financial crime. Adversarial testing is a security evaluation method that involves actively attempting to break or exploit vulnerabilities in a system, particularly in AI and ML models. It involves simulating attacks to identify weaknesses and improve the robustness and security of the system. This proactive approach helps uncover potential flaws that might be exploited by malicious actors. The following screenshot illustrates experimentation tracking and a training loss plot in Amazon SageMaker Studio.

Deployment phase

In the development phase, AI systems move into production environments with careful consideration for confidence indicators and human review processes. Before live deployment, systems should undergo testing in operational environments with attention to localization needs across different regions.

In payment applications, deployers are encouraged validate performance, monitor concept drift as user behavior changes over time, and maintain version control with documented rollback processes to address unexpected issues during updates. Deployment includes establishing clear thresholds for human intervention, particularly for high-value transactions or unusual activity patterns that fall outside normal parameters, with localization for different markets’ payment behaviors and regulatory requirements.

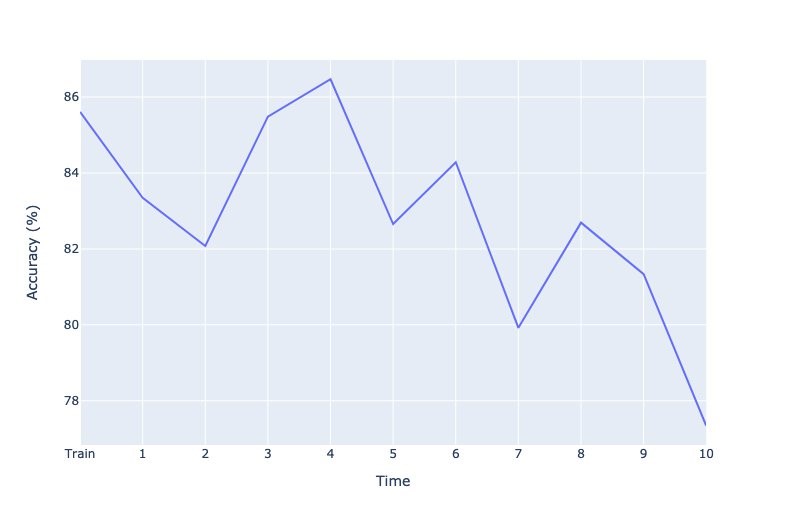

The following graph is an example of using Amazon Sagemaker Model Monitor to monitor data and model drift.

Operation phase

The operation phase covers ongoing system management after deployment. System owners should notify users about AI interactions, consider providing opt-out options, and maintain accessibility for the intended users. This phase establishes feedback mechanisms through in-system tools or third-party outreach for continuous and thorough testing for improvement.

The operation phase for payment AI systems includes transparent communication with customers about AI-driven decisions affecting their accounts. Continuous monitoring tracks concept drift as payment patterns evolve with new technologies, merchants, or consumer behaviors. Feedback mechanisms capture both customer complaints and successful fraud prevention cases to refine models. Safeguarding mechanisms like guardrails enhance safety by constraining inputs or outputs within predefined boundaries, ranging from simple word filters to sophisticated model-based protections.

The following are practical recommendations:

- Performance monitoring – Advanced monitoring frameworks track technical efficiency and nuanced indicators of fairness, transparency, and potential systemic biases. These systems create a continuous feedback loop, helping organizations detect and address potential issues before they become significant problems.

- Feedback mechanisms – Feedback in responsible AI is a sophisticated, multi-channel system. Rather than focusing on collecting data, these mechanisms can create dynamic, responsive systems that can adapt in real time. By establishing comprehensive feedback channels—from internal stakeholders, customers, regulators, and independent reviewers—organizations can create AI systems that are technologically sophisticated and responsive to human needs.

- Model retraining – Regular, structured model training processes make sure AI systems remain aligned with changing economic landscapes, emerging regulatory requirements, and evolving societal norms. This approach requires developing adaptive learning capabilities that can intelligently adjust to new data sources, changing contexts, and emerging technological capabilities.

Conclusion

The responsible use of AI in the payments industry represents a significant challenge and an extraordinary opportunity. By implementing robust governance frameworks, promoting fairness, maintaining transparency, protecting privacy, and committing to continuous improvement, payment providers can harness the power of AI while upholding the highest standards of responsibility and compliance.

AWS is committed to supporting payment industry stakeholders on this journey through comprehensive tools, frameworks, and best practices for responsible AI implementation. By partnering with AWS, organizations can expect to accelerate their AI adoption while aligning with regulatory requirements and customer expectations.

As the payments landscape continues to evolve, organizations that establish responsible AI as a core competency will mitigate risks and build stronger customer relationships based on trust and transparency. For more details, refer to the following Accenture report on responsible AI. In an industry built on a foundation of trust, responsible AI is a responsible choice and an important business imperative and success.

To learn more about responsible AI, refer to the AWS Responsible Use of AI Guide.

About the authors

Neelam Koshiya Neelam Koshiya is principal Applied AI Architect (GenAI specialist) at AWS. With a background in software engineering, she moved organically into an architecture role. Her current focus is to help enterprise customers with their ML/ genAI journeys for strategic business outcomes. She likes to build content/mechanisms to scale to larger audience. She is passionate about innovation and inclusion. In her spare time, she enjoys reading and being outdoors.

Neelam Koshiya Neelam Koshiya is principal Applied AI Architect (GenAI specialist) at AWS. With a background in software engineering, she moved organically into an architecture role. Her current focus is to help enterprise customers with their ML/ genAI journeys for strategic business outcomes. She likes to build content/mechanisms to scale to larger audience. She is passionate about innovation and inclusion. In her spare time, she enjoys reading and being outdoors.

Ana Gosseen Ana is a Solutions Architect at AWS who partners with independent software vendors in the public sector space. She leverages her background in data management and information sciences to guide organizations through technology modernization journeys, with particular focus on generative AI implementation. She is passionate about driving innovation in the public sector while championing responsible AI adoption. She spends her free time exploring the outdoors with her family and dog, and pursuing her passion for reading.

Ana Gosseen Ana is a Solutions Architect at AWS who partners with independent software vendors in the public sector space. She leverages her background in data management and information sciences to guide organizations through technology modernization journeys, with particular focus on generative AI implementation. She is passionate about driving innovation in the public sector while championing responsible AI adoption. She spends her free time exploring the outdoors with her family and dog, and pursuing her passion for reading.